Value Added Tax (V.A.T.)

Until 1940, Britons paid tax only on their incomes, but wartime shortages saw the introduction of a purchase tax too. It was not until our entry into the EEC that this was abolished, but another purchase tax called Value Added Tax (V.A.T.) took its place and it was brought into law by the Finance Act of 1972. Though it started at 10% it has been 20% since 2011 and constitutes around 15% of total government revenue.

The collection process is that an invoice is issued showing the sales price and underneath is shown the V.A.T., with a grand total under that. The business’s V.A.T. registration number, trading name and address must also appear. Every month, a V.A.T. Return is completed, giving the total V.A.T. paid out to other businesses and the total collected from customers. The difference is what is due to (or from) H.M. Revenue & Customs. In this way, the business is the intermediate tax-collector and the consumer is the one who pays the tax.

Governments up to 2011 varied the rate to suit their economic policies ~ low to stimulate spending, high to bring down inflation ~ making its historical record appear rather lumpy. Other adjustments have been to exemptions for ‘essentials’ and zero- and reduced-rate items.

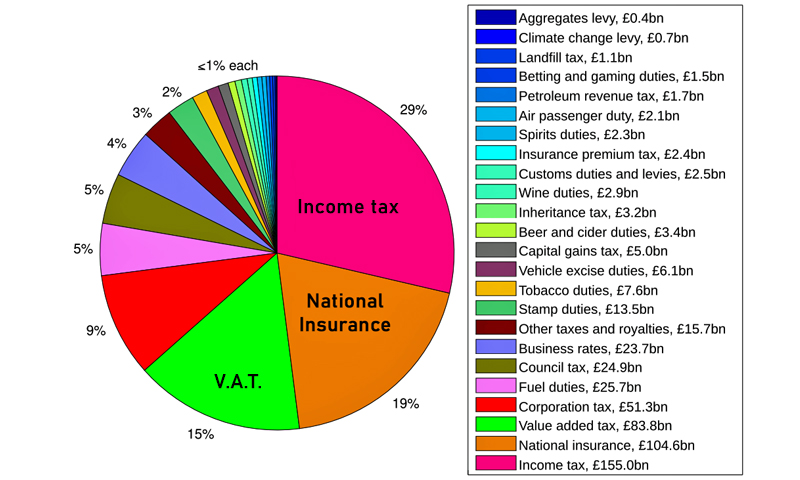

(Image showing UK tax revenue for 2008-09: Splash & Gamekeeper at Wikimedia Commons / CC BY-SA 3.0)